Machine-readable view

The AI and EV Driven Capacitor Shortage

2026-07-02T05:00:00.000Z · Ninad Kashid

Featured image: MLCC capacity market share

AI servers and 800V EVs are colliding with a structural capacitor shortage. MLCC lead times have stretched past 20 weeks, barium titanate supply is concentrated in China, and tantalum prices are climbing. Here's what's driving it, and how hardware OEMs can engineer the risk out of their BOM before it locks in.

The global supply chain for passive electronic components is undergoing a violent structural shift. As the cost of high-performance capacitors climbs to reflect a deepening supply shortage, a stark reality is emerging for hardware Original Equipment Manufacturers (OEMs): the rapid evolution of Artificial Intelligence (AI) and Electric Vehicle (EV) architectures is fundamentally breaking legacy component supply chains.

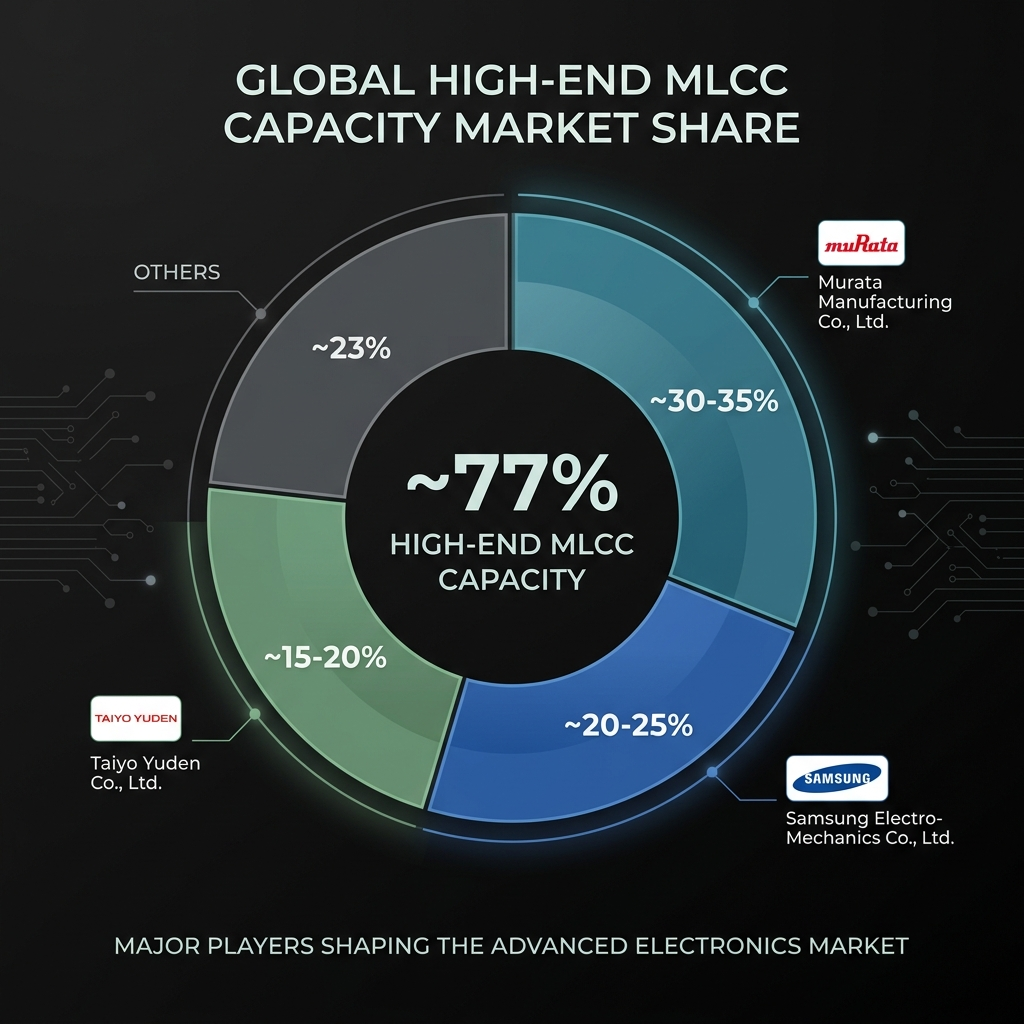

As of mid-2026, the market has bifurcated. Murata, Samsung Electro-Mechanics, and Taiyo Yuden control roughly 77% of global high-end MLCC capacity, running at 90 to 95% utilization with no spare room for demand surges. Lead times on high-capacitance parts have stretched from 6 to 8 weeks in late 2024 to 4 to 6 months today, and analysts expect the constraint to persist through 2027. For hardware engineering and procurement teams, reacting to a shortage after a BOM is locked is no longer viable. The instinct to stockpile "just-in-case" inventory only ties up capital in static stock while the underlying technology keeps moving.

To survive this volatility, OEMs must stop relying on scattered WhatsApp threads and Excel BOM attachments to chase parts, and start building supply chain visibility directly into the engineering workflow.

The Automotive Electrification Multiplier

The global push for emissions reduction has forced a complete redesign of the automotive Bill of Materials, creating immense upstream pressure on passive components.

The shift from internal combustion engines (ICE) to electric drivetrains has triggered a massive component multiplier. A standard ICE vehicle requires roughly 3,000 Multilayer Ceramic Capacitors (MLCCs). A modern EV equipped with Advanced Driver Assistance Systems (ADAS) and telematics can require up to 22,000.

This near seven-fold increase comes from converging systems. Vehicles now process real-time data from LiDAR, radar, and optical sensors, which requires dense arrays of high-reliability capacitors to stabilize power across the sensor suite. At the same time, OEMs standardizing 800-volt battery systems need larger, higher-voltage, more heat-resistant DC-link capacitors, since these components must be 20 to 30% larger to hold safety margins against electrical arcing. That single requirement shrinks the pool of qualified suppliers sharply.

The Strain of AI Infrastructure

Automotive electrification is not the only driver. The capacitor segment is straining to feed AI hardware at the same time.

AI servers require exponentially more decoupling and filtering capacitors per unit than traditional enterprise servers to manage heat and hold voltage stable. An Nvidia GB200 server uses approximately 6,500 MLCCs. The upcoming Rubin platform is expected to require around 12,000 per unit, 5 to 10 times the volume of a traditional server. AI servers account for only 2 to 3% of total MLCC unit volume, but they consume around 15% of high-grade capacity, squeezing allocations for every automotive and industrial buyer competing for the same constrained pool.

The Production Squeeze: Why Capacity Isn't Enough

Lead times on high-capacitance MLCCs have moved in three distinct steps. In late 2024, they ran 6 to 8 weeks. By early 2026, they had stretched past 20 weeks. By mid-2026, they extended further to 4 to 6 months, and analysts expect the constraint to persist through 2027.

A common misconception is that increasing factory capacity will stabilize prices. Overall global MLCC production volume is growing, but the type of demand has shifted, not the total. AI infrastructure and 800V EVs require high-spec, high-voltage, high-temperature components that take longer to manufacture and yield lower pass rates than standard consumer-grade parts. That is a structural bottleneck, not a capacity problem, and new high-grade fabs take 1.5 to 2 years to build plus 12 or more months for equipment ramp and yield optimization.

The bottleneck is compounded further upstream. High-end MLCCs rely on barium titanate as the core dielectric material, and it accounts for roughly 70% of an MLCC's raw material cost. Over 70% of high-purity barium titanate refining capacity sits in Chinese state-controlled enterprises. Automotive and AI-server grade MLCCs additionally require doping with heavy rare earth elements, dysprosium and terbium in particular, and over 90% of the world's high-purity heavy rare earth separation and refining capacity is also concentrated in China. That is two single-source chokepoints stacked on top of each other, both exposed to export-control risk, not just raw scarcity.

Tantalum is not a safe alternative. Panasonic announced price increases of 15 to 30% on certain tantalum capacitors effective February 2026, and design teams are increasingly forced into hybrid tantalum-plus-MLCC solutions, which pushes even more demand back onto the constrained MLCC pool. Costs across specific categories are moving as a result:

High-Capacitance MLCCs: AI-grade and automotive-qualified (AEC-Q200) versions are under strict allocation, with Murata raising prices 15 to 35% on AI server and high-end automotive grades in a single round in 2026.

Tantalum and Polymer Capacitors: Critical for AI server power rails. Structural price increases are compounding on top of an already tight raw tantalum supply chain.

Electrolytic and Film Capacitors: Needed to manage load spikes in GPUs and EV drivetrains. Prices are firming as manufacturing capacity for high-voltage grades stays constrained.

Engineering Risk Out of the BOM

When the market tightens this severely, traditional procurement methods fail. You cannot offset rising capacitor costs and sudden End-of-Life notices by manually searching distributor directories, chasing brokers over WhatsApp, or attaching a BOM to an email and waiting three weeks for quotes to trickle back.

Lexa closes that gap at the point where a BOM becomes a quote. Upload a BOM and Lexa extracts every line item, then matches it against a network of Lexa-verified manufacturers, weighted across availability, price, lead time, and quality, with a full quote turnaround inside 24 hours. High-risk or custom parts route through a deterministic capability match plus a written AI Sourcing Audit, so your team gets documented reasoning behind every recommended alternate, not just a number.

Every step from extraction to delivery is logged in Journey View, a tamper-evident, timestamped record with actor attribution. When a part goes on allocation or a supplier misses a commitment, you have a defensible trail instead of a guess, and your own confidentiality is protected structurally, since even your approved supplier list sits behind an NDA gate.

This is not a dashboard bolted onto a broken process. It runs on five years of live procurement operations across ₹285 crore of managed spend in Aerospace, Mobility, Robotics, Defence, and Energy, where these exact shortage dynamics were solved by hand before they were built into software. Your procurement team should not be acting as data entry clerks chasing allocated parts. Let Lexa handle the mechanics.